Snijden met precisie na overname levert meer waarde op

Last modified: 20 juli 2023 12:17

Professor Killian McCarthy en Nynke Keuning laten in hun paper 'Post-Acquisition Downsizing and Firm Performance' zien dat er na de overname van een bedrijf meestal in de kosten wordt gesneden. Dat is op zich oké, als managers maar wel met precisie te werk gaan. Als er te veel personeel wordt ontslagen, wat niet zelden gebeurt, heeft dat uiteindelijk een negatief effect op de resultaten. Het artikel is geschreven in het Engels.

Mergers and acquisitions occur for a number of reasons.

Cost-cutting is one of the more important and more dependable of motives: scholars suggest that while only about 7% of revenue-expanding forecasts are realized after an acquisition – in terms of new sales etc – about 60% of cost-cutting forecasts are realized (Houston et al., 2001). This is because, clearly, costs are more easily cut than revenue are expanded, and one of the most easily cut costs are human costs. Almost all acquisitions, therefore, lead to substantial employee downsizing, or even mass layoffs (Siegel and Simons, 2006; Lehto and Böckerman, 2008).

Theoretically this is a good thing: downsizing can be used to eliminate costly and unnecessary management layers and bureaucracy, which are often reasons for delay in decision making (Shook and Roth, 2011). Downsizing can also be used to reduce operating costs (De Meuse et al., 2004), to streamline operations and to improve the effectiveness of the firm, which all improve competitiveness (Espahbodi et al., 2000; Wayhan and Werner, 2000).

Practically speaking however, downsizing is often not as simple and surgical as it sounds. For starters, the acquiring firm often has difficulties in identifying what to downsize. And in downsizing the acquiring firm often ‘kills the goose that lays the golden eggs’: by dropping the wrong people, the acquiring firm creates uncertainity, teams fall apart, ‘the good people’ leave, productivity drops, and the dynamics of an organization change (Marks, 2003; Shook and Roth, 2011).

In other words, an acquirer makes an acquisition because the target firm does something better, but in integrating that acquisition the acquiring firm so badly damages the target that it can no longer do what it used to do so well. The result is a sort of buy-and-break effect, which means that the financial benefits of downsizing remain, at best, unclear (Conyon et al., 2002; Love and Nohria, 2005), and so the use of downsizing as a tool for creating value remains controversial (Wayhan and Werner, 2000; O’Shaugnessy and Flanagan, 1998).

The empirical evidence on downsizing – as with most of the empirical literature on the performance of mergers and acquisitions – comes from the study of Anglo-Saxon and, more often than not, US acquirers. The US / Anglo-Saxon world, however, has a distinct way of doing business, and of dealing with people which is not necessarily generalizable, for example, to Dutch acquirers operating in the Continental system, or to Japanese acquirers operating in the Confucian system. There are gaps, therefore, in our understanding as to whether it is downsizing that destroys value, or whether it is downsizing by American / Anglo-Saxon acquirers that destroys value.

It is this observation that motivated this study. We build a sample of 3,267 large mergers and acquisitions, spanning a 27 year period (1986 – 2012), including firms which range from a very small amount of employees (1 FTE) to a very large numbers of employees (471,755 FTE), from a wide range of industries, and a wide range of regions.

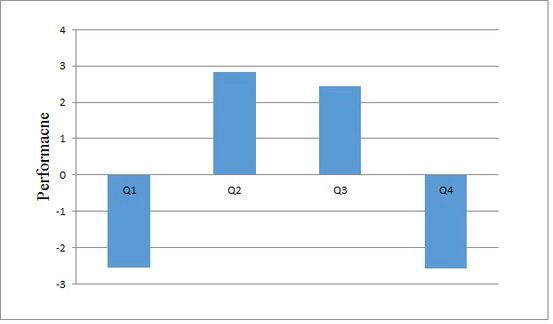

Figure 1 – Results for ROA, amount of employees downsized by firms in the sample

We find:

– In the sample of 3,267 firms, 73% downsized because of the acquisition. The remainder expanded their workforces after the acquisition. These firms downsized, on average, 2,992 FTEs with each acquisition.

– Downsizing the target after the deal did not impact the performance of the acquiring firm.

– Downsizing the acquiring firm, in the year before the deal, has a positive significant. We split the downsizing acquirers into quartiles. The firms in the sample, which performed best in the year after the deal, downsized between 85 and 96 employees; on Figure 1, these, are the firms in the 2nd and 3rd quartile. Those in the 2nd quartile improved performance (measured by return on assets) in the year after the acquisition by 2.84%. Given that the mean firm in our sample had 25,452 employees, the suggestion is that small, surgical incisions are better. When the average firm in our sample cut more than 96 FTEs, it destroyed value.

– Looking at a number of cultural clusters – the Anglo-Saxon cluster, which includes British and American acquirers, the Germanic cluster, which includes Dutch, German and Scandinavian acquirers, the Latin cluster, which includes Latin America, and Latin Europe, and the Confucian cluster, which included China and Japan – we find that only Germanic firms can create value from downsizing in the year after the deal.

The results from our this research are interesting and significant. They suggest: (1) managers should look to cutting costs in their own firm before they start cutting into another; (2) only small precision cuts are necessary, and large, deep cuts only serve to bleed performance; (3) Germanic managers are able to create value with downsizing, while others aren’t, and so there are lessons to be learned from the Germanic world.

Additional research is required to consider: (1) industry specific effects; (2) the speed of the downsizing; and (3) to gain insights into what it is that managers in the Germanic system are doing so differently to managers in the other systems. For now, however, the lessons from these 3,267 acquisitions are rather clear.

Nynke Keuning completed her Masters in Strategic Innovation Management at the University of Groningen in 2015. She is currently searching for a job in field.

Killian McCarthy is both an Assistant Professor in the Economics of Strategy at the University of Groningen, and the Director of the Masters Programme Strategic Innovation Management . He completed his PhD thesis in 2011 on the performance of international mergers and acquisitions.