Management Incentive Plans (MIP’s): ‘A chance to distinguish oneself’

Question 1: Wat is a MIP?

MIP stands for Management Incentive Plan and refers to a plan which is often implemented when a company is purchased by a Private Equity firm. The aim of a MIP is to align the interests of company management with the interests of the PE firm. This is done by asking management to also invests in the own company. Often management’s investment in shareholder loans and/or preference shares is bigger than their investment in ordinary shares, but the % of ordinary shares they acquire is often higher. This way management has an incentive to increase the value of the company so that they will benefit when the company is sold at a higher value.

Question 2: What makes a MIP special?

Compared to buying shares on the stock market, a MIP has a higher risk profile, because it combines a bigger chance to lose money and to get a higher return. Even compared to the PE firm, the investment by management has a higher risk profile. This is because of the additional ordinary shares (so-called ‘Sweet’ equity) management can acquire as part of the MIP, next to the ‘Strip’ investment management makes under equal conditions as the PE firm.

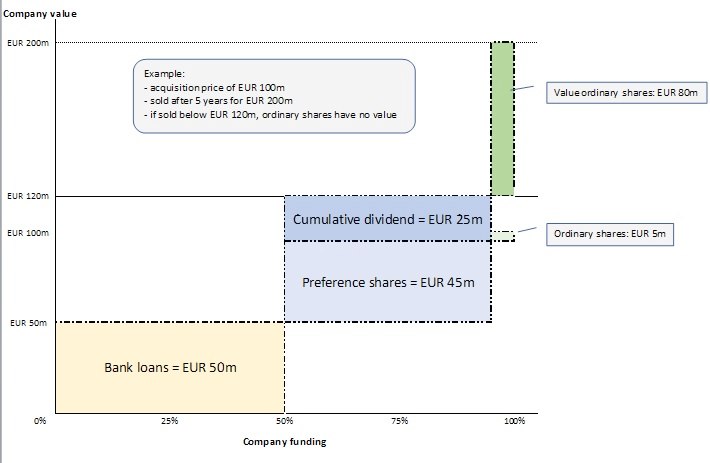

Question 3: How does this work?

When a company is sold, first the debt is repaid in order of seniority. Subsequently, the preference shares are repaid including the cumulative dividends. After that, if there are sales proceeds remaining, these are distributed over the ordinary shares. Therefore, an investment in ordinary shares has a relatively high chance to be worthless, but also a relatively high chance to be very lucrative, which makes the risk profile comparable to a share option.

Simplified presentation of the value of ordinary shares

Question 4: How does the Dutch Tax Authority look at this?

In case management acquires shares for a value lower than their economic value, a wage tax risk arises over the difference. If no certainty in this matter is obtained upfront based on agreement with the Tax Authority, this can lead to a high tax assessment afterwards. This is because the Tax Authority can decide to estimate the economic value of shares at the time of purchase based on the realized sales proceeds. This approach will lead to a relatively high estimated economic value, because the upfront risk exposure is then no longer taken into account.

The chance to reach an agreement with the Tax Authority upfront increases if during the MIP design, even before management invests, acceptable risk-return ratios are taken into account. Moreover, it is important to properly substantiate the value of preference shares and ordinary shares e.g. by making use of an Option Pricing Model approach.

Question 5: So there is a tax risk at purchase, what happens at sale?

Taxation differs from country to country. The balance between stimulating management on the one hand and the tax consequences on the other hand is sometimes hard to find, but is very important for Private Equity firms and management of the acquired company. When it concerns a transaction in The Netherlands, a MIP often constitutes so-called lucrative interests. This means that the sales proceeds are in principle taxed as result in Box 1 (49.50%). However, if the MIP is structured properly, the benefits from lucrative interests can be taxed as income from substantial interests in Box 2 (26.25%).

Question 6: How important is a MIP for deal success?

The importance of a MIP can be very big, especially when there are multiple interested buyers. When interested buyers make comparable offers, eventually not only the takeover bid and the provisions in the Sales & Purchase Agreement (SPA) are leading. In case of an acquisition, experience and track record of the Private Equity firm in the sector will be important for the credibility of their investment case. The MIP reflects how this turns out financially for the different investors, including management. Therefore, the MIP forms an important part of the deal. A Private Equity firm can distinguish itself positively by designing the MIP properly and ensuring it is as effective as possible.

Question 7: What makes a MIP effective?

That depends on several factors. Apart from the tax perspective, the MIP should be effective from a reward perspective, which means getting and keeping the interests of management aligned with the interests of the PE investors. An effective MIP is fair and fully understood by all parties. This can be ensured by modelling the MIP in such a way that the financial impact of design choices and different scenarios can be made clear.

Eventually the PE firm and company management have the same interests, but before the MIP terms are agreed, negotiation takes place on the distribution and conditions. An effective consultation process can take place if there is trust from both sides, which strongly depends on the level of transparency about the MIP and the exit strategy.