M&A: Dutch buyers acquiring less international despite globalization

Last modified: 20 juli 2023 12:25

Magdalena Langosch en Dr. Killian J McCarthy, onderzoekers aan de Rijksuniversiteit Groningen, komen in een Engelstalige paper tot een belangwekkende conclusie: Nederlandse partijen doen minder overnames in het buitenland, ondanks dat de wereld economisch is geglobaliseerd. En als Nederlandse kopers een acquisitie doen, is dat meestal in West-Europa.

Introduction

Half way through the second decade of the 21st century, and using a sample of 8,629 Dutch acquisitions, completed since 2000, the aim of this article is to reflect on what Dutch dealmakers have been doing, to see what sort of trend might be emerging. We find:

1. The number of deals remains sensitive to macroeconomic conditions

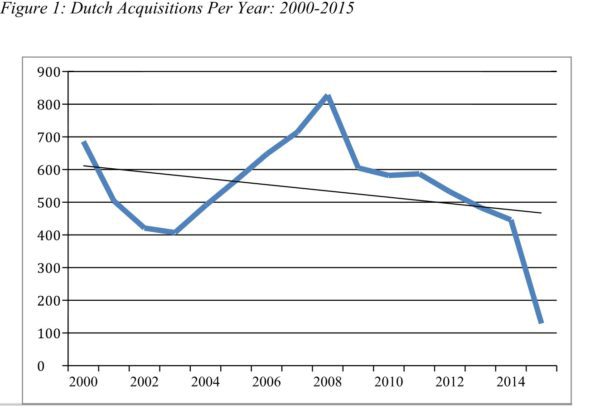

There were 8,629 acquisitions involving Dutch firms since 2000. Between 2003 and 2008, the number of deals involving Dutch acquirers increased significantly. It peaked in 2008, with 828 acquisitions per year, at the high point of what has been termed the 6th wave (McCarthy, 2011), and declined significantly as the financial crisis unfolded. After 2008, year on year, the number of Dutch acquisitions fell by over 200 in 2009 and the market, it appears, has yet to fully recover. Between 2010 and 2014 the market shrunk by 23,37 percent. The first half of 2015 showed a 42,15 percent decrease on the same period in 2014, suggesting an overall decreasing trend (see Figure 1). It seems, in other words, that the merger market has still yet to fully recover after the Financial Crisis of 2008-10.

2. Percentage acquired stays relatively constant over time

Of the 8,629 acquisitions, 5,381, or 62.36 percent of the total, were 100 percent acquisitions. The share of 100 percent acquisitions per year is relatively stable over time.

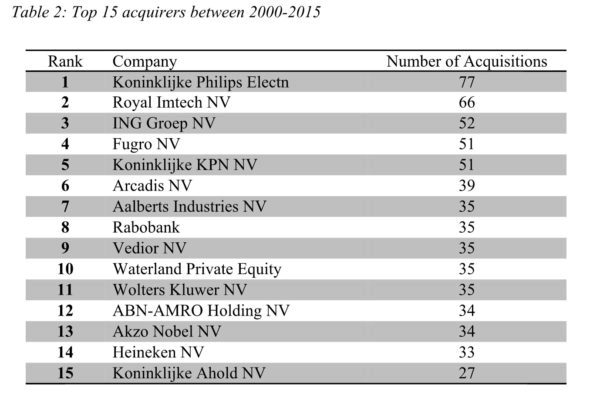

3. Top acquirers miss important Names

Since 2000, Philips (77 acquisitions), Royal Imtech (66) and ING Groep NV (52) made the most acquisitions, which is in itself not a surprise itself. Over 95 percent of Philips’ acquisitions was were international but, echoing the declining willingness of Dutch acquirers to cross border, Philips has only made 5 international acquisitions in the past three years, all of which were completed in 2014. International shares for deals made by Royal Imtech and ING Groep are both somewhat smaller, at 80 and 85 percent respectively. Interesting findings here refer to the fact that the trend for ING Groep is significantly down sloping whereas Royal Imtech tends to increased deals over the years.

Also interesting, is the big names not in the top 10. Heineken, for example, is only ranked 14, with 33 acquisitions in 15 years, despite claiming to have an acquisition culture, and Royal Dutch/ Shell Group is ranked 92 having only closed 10 deals between 2000 and 2006. The upcoming merger between Shell and BG Group, announced in April 2015 and planned for 2016 (Reuters, 2015), therefore, will be its first significant deal in 9 years.

4. International ‘real M&As’ show decreasing trends

The willingness of the Dutch to cross borders has seesawed throughout the period, but demonstrates a clearly decreasing trend. In 2000, over 50 percent of Dutch 100 percent acquisitions were cross-border deals, and in 2001 almost 60 percent of Dutch deals involved cross-border partners. Between 2002 and 2004, however, the number of Dutch cross-border deals dropped by 23 percent. Why is somewhat of a mystery: in 2002-2004, the global economy was growing strongly, and the cash to finance acquisitions was readily available.

Despite this, it seems that Dutch firms decided not to cross the border. After 2004, the share of cross border deals increased again, but collapsed further after the Financial Crisis, with the low point in 2009 when only 32 percent of Dutch deals involved cross-border partners. Since 2009, the share has again increased, but nothing to the point that it was at the beginning of the century. The trend, in other words, is for a declining number of Dutch deals to involve cross-border partners. Understanding why is important. From a performance perspective, given that cross-border deals perform less well, this is a welcome finding. From a strategic perspective, given that cross-border deals bring new knowledge and provide access to new markets, the decreasing willingness of Dutch firms to cross the border is somewhat more troubling.

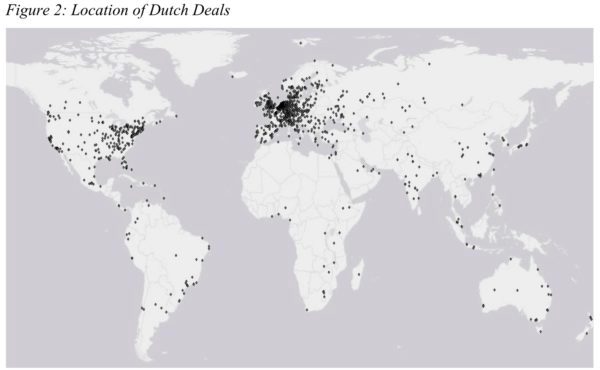

5. Majority of International Trends remain within Europe

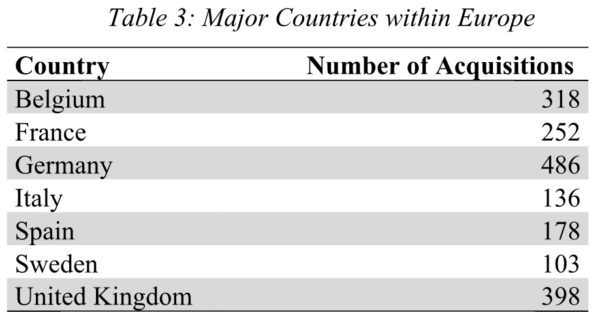

Looking at where the Dutch have internationalized to, provides some additional insights. Figure 2 plots the location of Dutch cross-border targets. It shows that: (1) that the overwhelming majority of Dutch deals remain in Europe. The distribution of European deals range between 55 percent to over 70 percent of total international deals made. (2) Outside of Europe, the safety of North America, and the United States in particular, are draw significant Dutch investment. (3) The most talked about BRIC Countries – Brazil, Russia, India and China – attract far less investment then might have been expected. It shows that Dutch acquirers are not particularly risk loving when choosing targets. Table 3 reiterates this fact, and shows that the Dutch internationalize within their back yard.

6. Deals outside Europe still show slightly increasing trends

Event though we concluded that the majority of deals remain in Europe, looking at destinations outside Europe provides an interesting view as well. Trends for deals outside Europe possess a rather increasing line looking at country groups such as BRIC – Brazil, Russia, India and China – or Next Eleven –Bangladesh, Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, Philippines, Turkey, South Korea and Vietnam – even though their average share on the total numbers of international deals are relatively low with 10.06 percent and 5.27 percent respectively. Regarding China, as included in the BRIC clustering in the analysis, on average 25 percent of total acquisitions were done there, indicating a relatively balanced distribution within the country group.

However, with a total number of 115 deals within 15 years, thus 7 to 8 deals per year, the numbers are lower than media might lead us to believe. Surprising development of the country is seen in the year 2014, where the number of acquisitions jumped significantly from an average of around 5 deals in the years before (2000-13) to 48 in the following year (2014), which indicates a share of over 70 percent of acquisitions made in the BRIC region and 22 percent of all international deals for that year. The latest numbers thus lead to questions regarding the reasons for such a significant change and development towards China as well as curiosity regarding the development over the upcoming years.

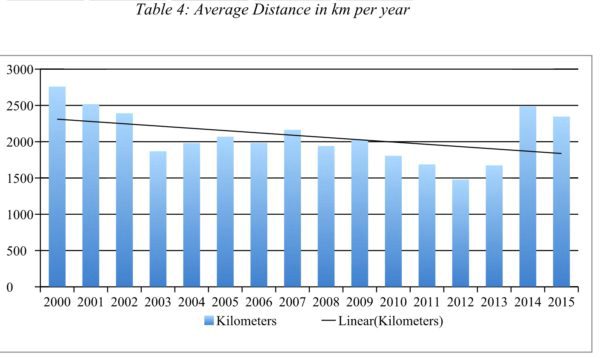

7. Average Distances somewhat contradict Trend Lines

Lastly, we considered the average distance, measured in kilometers, that the Dutch acquirers were willing to travel in order to make an acquisition every year. As we discussed, international deals in general follow a decreasing trend and thus it is no surprise that average distances follow such a negative trend as well. In general the average distances over the past 15 years, Dutch acquirers were willing to travel, is about 2,074 kilometers, the distance from Amsterdam to Helsinki or Tallinn.

The average distance ranges between 2,769 km in 2000 as the highest point and 1479 km in 2012 as lowest point, indicating the willingness to leave the Netherlands but not really Europe. Regarding the fact that the trend for deals outside Europe are increasing to some extent, we would expect the distance at least on average to be on a slightly more increasing trend as well, especially regarding the BRIC and Next Eleven countries, which are located in South America and Asia. Despite those considerations, one may raise questions, why Dutch acquirers, the successors of great internationalizes, such as the VOC, are keeping the distance rather low in times of globalizations and internationalization.

Conclusion

These results suggest: (1) the Dutch are making fewer deals; (2) that a smaller share of Dutch deals is international; and (3) that the Dutch are choosing to stay in their back yard. From an acquisition performance perspective, this is a positive thing: most acquisitions fail, international acquisitions are more likely to fail, and exotic international acquisitions are particularly risky. By focusing so much on doing it ‘safely’, however, by doing fewer deals, and more local deals, it may be that Dutch acquires, in the longer term, miss out on opportunities to acquire new knowledge, new resources, and to gain access to new markets. There is a risk/reward trade-off. And in the globalized 21st century, the preference of Dutch acquirers seems to be for a low-risk / low-reward and may not be enough in the long-run.

The authors

Magdalena Langosch is Research Assistant at the University of Groningen and a Master student at the Rotterdam School of Management. She obtained her Bachelor degree in International Business from the University of Groningen. Her research interests focus on cross-cultural Management, post-acquisition integration and Knowledge Management.

Dr. Killian J McCarthy is an Assistant Professor in the Economics of Strategy at the University of Groningen, and the Director of the Masters Program Strategic Innovation Management. He completed his PhD thesis in 2011, for his study of the performance of 35,000 international mergers and acquisitions from Asia, Europe and North America.