There’s significant evidence that Dutch buyers fail in non-European acquisitions

Last modified: 20 juli 2023 12:26

De tweede paper van het M&A-onderzoek van Magdalena Langosch en Dr. Killian J McCarthy, onderzoekers aan de Rijksuniversiteit Groningen, gaat over de performance van Nederlandse overnames in het buitenland. Vooral buiten Europa blijkt deze significant slecht te zijn. Dat is zonde want juist de economieën buiten Europa groeien hard.

Magdalena Langosch en Dr. Killian J McCarthy onderzoeken de stand van M&A in Nederland sinds het jaar 2000. De vorige keer schreven zij in hun eerste paper dat Nederlandse kopers in steeds mindere mate hun aqcuisities in het buitenland doen. En als zij dat al doen, meestal in de achtertuin, oftewel België, Duitsland en Frankrijk. Hier volgt een tweede artikel uit het onderzoek.

The resarch

Dutch acquirers announced 8,629 acquisitions since 2000. How did these perform? And what performance trends can be discerned? This article considers these questions.

We calculate performance for 2,777 of the 8,629 acquisitions – these represent 100% of acquisitions announced by public acquirers in the period which report the necessary details – and we measure performance using an ‘event study’ methodology – a stock-market based performance measure which describes performance by comparing the firms actual stock market value, after the deal, with its expected value, in the absence of the deal, controlling for industry-wide performance across 47 different stock exchanges. We find:

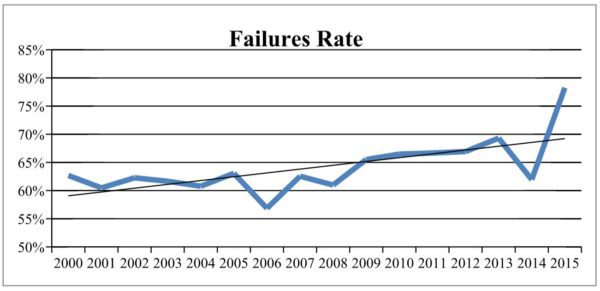

1, Failure Rates remain high

Our sample shows that a majority of 1,746 deals are failures and only 1,031 are categorized as successful in terms of achieving values greater than zero. The general percentage distribution is thus, 62.89 percent failures and 37.11 percent successes over the past 15 years, showing that deals are less profitable for Dutch Acquirers than expected in the last two decades. Looking at the shares of failures of each year, we see a small but continuous increase, predicting a low performance in the upcoming years.

2, Domestic Failure vs. International Failure is almost equally high

International Business research warns us that cross-border acquisitions are the major source for failures in the M&A market in times of globalization. We find little support for that suggestion, however, and show that domestic and international deals fails at roughly the same rate: 62,07 percent of Dutch domestic deals in the past 15 years were considered failures, and 63,23 percent of Dutch international deals failed. This is surprising: the international deals involved targets in 86 countries, and despite the challenges that crossing the border brings, it seems that only 1.16 percent more international deals failed.

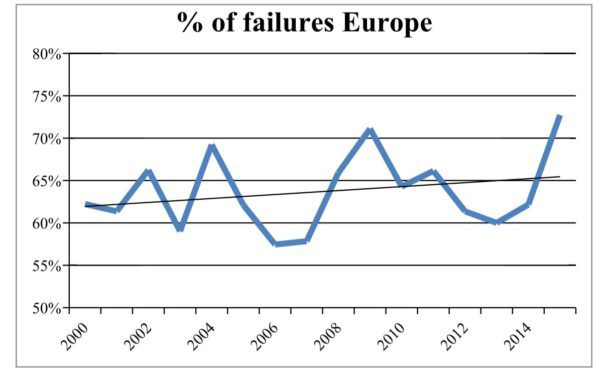

3, Failure Rates in Europe still higher than expected

In our previous article we showed that most Dutch deals remain in Europe. Looking at Europe, however, we see that failure rates remain high: between 57 percent (2006) and 73 percent (2015) of Dutch European acquisitions fail. What is more, the trends are still slightly increasing, not promising an improvement in the upcoming years for the Dutch. Thus, while Dutch acquirers may prefer to stay within Europe, assuming Europe is safer, and therefore assuming that performance is higher, this is not the case in reality.

4, Major Target countries don’t necessarily provide a safety net

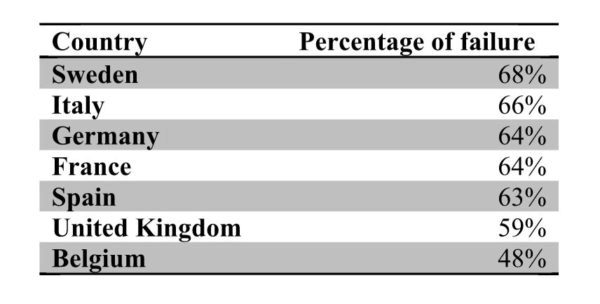

In Europe, most Dutch acquirers remain in the ‘back-yard’ — that is, in the closest of the European countries – presumably because ‘backyard’ destinations are thought to be safer. Again, however, the evidence is that ‘backyard’ countries do not always provide a very stable safety net. Belgian targets are the most likely to succeed, with a 48 percent failure rate, followed by the UK, with a 59% failure rate. Both, curiously therefore are safer destinations than the Netherlands for Dutch acquirers. The others – Spain, France, Germany, Italy and Sweden – are less safe than the Netherlands, and acquisitions into these countries are more likely to fail than the average Dutch international deal.

It is interesting to note too that of the seven, only two — Belgium and Italy — showed a positive development regarding overall acquisition performance; an increasing number of deals succeed in these countries each year. This might mean that Dutch acquirers are learning how better to do business in these countries, or that these countries have become increasingly attractive investment destinations. By contrast, Germany, UK and Sweden, offer stable returns in the period, while Spain and France offer decreasing returns.

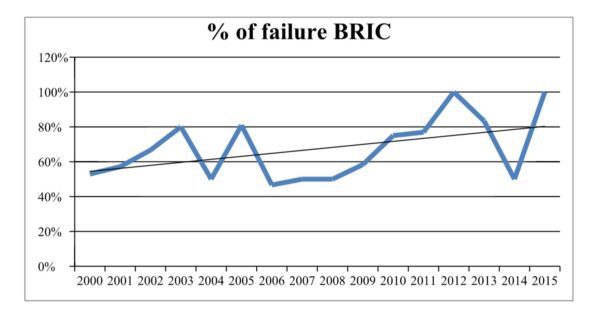

BRIC countries are not as promising as expected

Much talked about in the media, our analysis shows that 108 out of 167 acquisitions into the BRIC countries are classified as failures (2000-2015). The highest failure rates were identified in Brazil with up to 84 percent of Dutch deals destroying value, followed by China, with 71 percent. Our analysis shows that especially at the beginning and during the 6th merger wave (2003-2008) failure rates reached up to 80 percent and more.

These results contradict the popular belief: (1) that the BRIC countries offer better returns to an investment in slow-moving Europe; and (2) that China, in particular, is a certain bet.

Interesting however, is that contradicting to Europe, where failure rates reached the highest points during the financial crisis, results in the BRIC countries are surprisingly low in comparison. In fact failure rates around that period are marked as lowest in the entire analysis, leading to some questions for reasons for such a development.

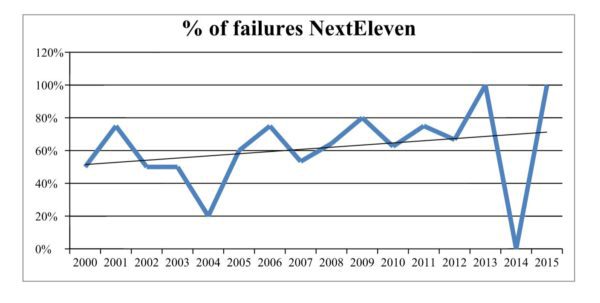

Next Eleven remain as a challenge

The so-called ‘Next Eleven’ – Bangladesh, Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, the Philippines, Turkey, South Korea and Vietnam – were identified by Goldman Sachs as high potential markets for the 21st century. Dutch acquirers have been slow to enter these markets and, failure rates remain high. We find that up to 80% (2009) of Dutch acquisitions in the Next Eleven failed and, what is more, we show that the failure trend is increasing, demonstrating that Dutch acquirers are not learning how to do these deals better. If the Next Eleven are the next big thing, this is bad news.

Conclusion

In this article we show that failure rates for Dutch acquisition remain high, irrespective of where the target is located. M&A, in other words, continue to be a high-risk activity.

In our first article, we showed that Dutch acquirers prefer to stay local: in the Netherlands, in the Dutch back yard, or in Europe. This would seem to contradict the popular impression that firms have been directing their attention to emerging markets, in search of new growth, and would seem to suggest that Dutch acquirers are actually not big on internationalization.

In this study, we showed that, from a performance perspective, the Dutch hesitation to travel makes sense: the further the deal, the lower the performance. Belgium targets perform best. From a risk-based, accounting perspective, therefore, what the Dutch are doing is logical.

From a longer-term strategic perspective, however, this Dutch prudence remains questionable. If, as we are lead to believe by the economists, the BRIC countries and the Next Eleven, in particular, are to become the engines of 21st century growth – as opposed to Belgium – then Dutch acquirers need to improve their performance in those markets. Yes, targets in these countries are more complex, due to cultural and institutional differences, and thus more risky. But these risks can be reduced through proper integration planning and training. Because, simply put, if the growth is there, and we can’t do deals there, then we’ll miss the party.