Cross-border overnames vernietigen waarde

Last modified: 20 juli 2023 12:16

Bedrijven kunnen beter thuis blijven. Bij de meerderheid van cross border deals daalt de waarde van bedrijven. Verwachte voordelen als gevolg van het aanboren van nieuwe markten of resources kunnen de daling temperen of teniet doen. Dat concludeert wetenschapper Killian McCarthy op basis van onderzoek. Dit artikel is in het Engels geschreven.

Complication and disappointment

If there is one thing that scholars and practitioners, from a wide range of fields agree upon, its that internationalisations — crossing borders — leads to complication and disappointment.

Firstly, the economists tells us that distance increases transaction, monitoring, agency, and asymmetric information costs, while at the same time reducing the benefits of soft information (Grote and Umber, 2003; Böckerman and Lehto 2003; Hauptman and Hirji 1999; Cummings, 2007; Von Hippel, 1994; Morgan, 2004; Jaffe et al., 1993; Keller, 2002; Maurseth and Verspagen, 2002; Greunz, 2003; Storper and Venables 2004). These ‘costs’ — the so called costs of doing business ‘far away’ — imply that distant acquisitions are less likely to create synergies, and more likely to create difficulties.

Secondly, the international business scholars tell us that internationalisation creates ‘cultural’ and ‘institutional’ barrier to performance. Cultural distance — that is, the distance between what we do and what they do — and institutional distance — that is, the gap between the way our country is run and theirs is — complicates communication (Kaurent, 1983; Chevrier, 2003), creates uncertainty (Reus and Lamont, 2009), and leads to situations of ‘them and us’ in the work place (Huntington, 1993), which increases employee turnover (Krug & Hegarty, 1997). These ‘costs’ — the so called costs of doing business ‘internationally’ suggest that that foreign acquisitions are more likely to create difficulties.

Finally, the financial scholars support the suggestion that, empirically, its best to stay close, and to stay home. Chatterjee and Aw (2000), Eckbo and Thorburn (2000), and Moeller and Schlingemann (2005), for example, compare the performance of domestic and cross-border deals, in the case of UK, Canadian, and US acquirers, respectively, and show that domestic deals out-performance international ones, while Gozzi et al. (2008) finds that the value of a firm decreases after an expansion, and others have shown that any financial gains to deals which expand the geographic reach of the firm are, at best, ‘transitory’ (Sarkissian and Schill, 2008; Levine and Schmukler, 2006; Rossi and Volpin, 2004).

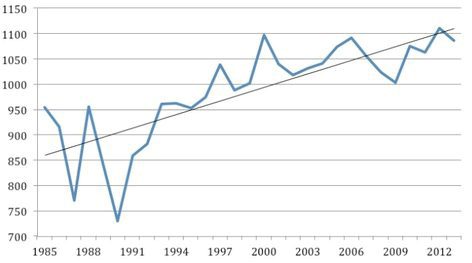

So why then are an increasing number of acquirers willing to increase the geographic reach of the firm (see Figure 1), and why do so many deals internationalise the firm? Using a sample of 4,223 acquisitions, completed in the period Jan 1 2000 to Dec 31, 2010, we explored this question.

Figure 1 – Average Geographic Distance: 1985-2012

We argued that there are three reasons to make a distant or cross border acquisition: a search for (1) market-based synergies — insofar as differences in the competitive of our market and theirs creates opportunities to gain — (2) non-market based synergies — insofar as insofar as political, legal, or fiscal differences between our market and theirs creates opportunities to gain — and / or (3) resource — insofar as the target firm offers or owns resources that creates opportunities to gain. We found:

1. Geographic expansion destroys firm value

Announcing a geographic expansion — be it for a distant or a foreign target — causes, all else equal, the market value of the acquiring firm to drop by 0.6%. Given that the average firm in our sample was worth $500 million, 0.6% equates to a drop in the market value of $30 million.

2. Resource-based objectives significantly moderate the performance of the deal

We find that differences in the resources of the target firm predict the way in which the market responds to the announcement of the deal. We find, for example, acquiring a distant target with a large market share causes the market to add to the value of the acquiring firm, rather than punish it.

3. Market-based objectives significantly moderate the performance of the deal

We find that the levels of competition in the home market impact the way in which the market responds to the announcement of the deal. Specifically, we find that if the levels of competition in the home market is high, then manager is rewarded for stepping out of this market. We expected to find, but did not find, evidence of a ‘pull’ to match this ‘push’ factor. We expected to find that host market concentration would impact performance, but failed to support that suggestion.

4. Non-Market-based objectives significantly moderate the performance of the deal

We find that differences in the tax, political and legal system impact the way in which the market responds to the announcement of the deal. Specifically, if the taxes are lower, if the politician come from a different political background (left versus right), and if the legal system is less burdensome (in terms of the financial and environmental requirements it places on the firm), then the market is less likely to apply the sort of punishment that is observed in the general case of a geographic deal.

In doing so, we demonstrate that while doing abroad and going far away causes problems, and is generally punished, the market is reasonable in the way in which it responds to the announcement. If the acquisition offers the acquiring firm market-, non-market, and / or resource-based gains, then the punishment can be lessened, or even dropped. In a world of ever more distant acquisitions, and ever more cross border deals, its good to know that at least in some cases, value is being created.

References – available upon request

About

Dr. Killian McCarthy is assistant professor bij de University of Groningen. Hij behaalde zijn PhD in economics of corporate strategy in 2011, voor zijn onderzoek over overnameprestaties. In dit onderzoek evalueerde Killian de prestatie van 35,000+ deals in Europe, Noord-Amerika en Azië in de periode 1990-2010.